Discover the role of fee-only model advisors in wealth management. Learn how their unbiased advice can maximize your financial success!

The Role of Fee-Only Model Advisors in Wealth Management

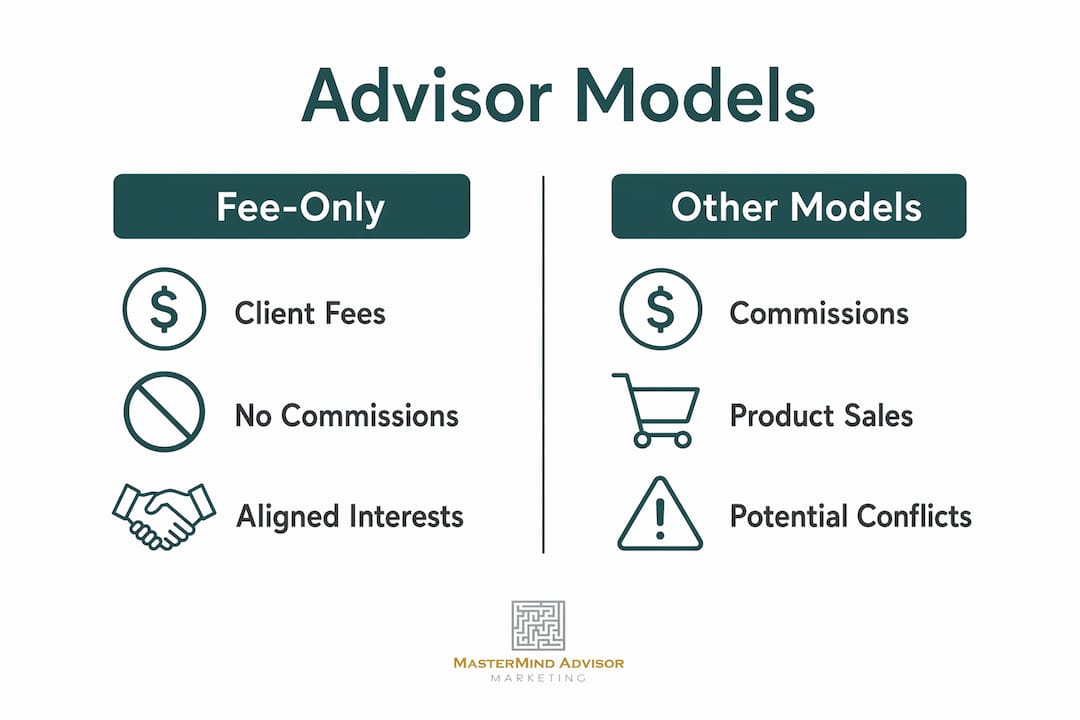

Fee-only model advisors are financial professionals compensated exclusively by their clients through direct fees, with zero commissions or third-party payments accepted. This compensation structure is the defining characteristic that separates them from the majority of advisors in the financial services industry. When your advisor earns nothing from product sales or trading activity, their recommendations serve one purpose: your financial benefit. Understanding this distinction is the first step toward making a genuinely informed choice about who manages your wealth.

How fee-only advisors' compensation models work

Fee-only advisors are compensated only by client fees and do not receive commissions or third-party payments. That single fact reshapes every conversation you have with them. There are no hidden revenue streams influencing which fund they recommend or how often they suggest you rebalance your portfolio.

The three most common fee structures are:

- Assets under management (AUM): The advisor charges a percentage of the total portfolio value they manage, typically between 0.5% and 1.5% annually. This model ties advisor revenue to portfolio growth, which broadly aligns incentives.

- Hourly rates: You pay for time spent, similar to hiring an attorney or accountant. This works well for one-time financial planning questions or specific project-based advice.

- Flat or retainer fees: A fixed annual or monthly fee covers an agreed scope of services. This model suits clients who want ongoing planning without a large investment portfolio.

Each structure affects the nature of the advisor relationship differently. An AUM-based advisor has a financial reason to stay engaged with your portfolio over time. An hourly advisor is incentivized to work efficiently and only as long as needed. A retainer model creates predictable costs for both parties and supports long-term planning relationships.

The critical point is what none of these structures include: commission incentives to trade or sell products. Commission-based advisors may be incentivized to trade more frequently because each transaction generates revenue for them. Fee-only advisors face no such pressure. In fact, the fee-only model enables advisors to credibly recommend inaction or holding strategies, since there is no financial reward for unnecessary activity.

Pro Tip: When interviewing an advisor, ask directly: "Are you fee-only or fee-based?" These sound similar but mean very different things. Fee-based advisors can still earn commissions alongside client fees.

Why fee-only advisors align better with fiduciary duty

Two terms dominate this conversation: fee-only and fiduciary. They are related but not the same thing, and confusing them is one of the most common mistakes individual investors make.

Fee-only is a compensation structure, while fiduciary is a legal obligation. A fiduciary advisor is legally required to act in your best interests at all times, disclose conflicts of interest, and prioritize your financial goals over their own compensation. Fee-only advisors are commonly fiduciaries, but the two designations require separate verification.

Here is how the standards compare:

| Standard | What it means | Legal requirement |

|---|---|---|

| Fee-only | Advisor earns only client-paid fees, no commissions | No legal mandate; voluntary compensation choice |

| Fiduciary duty | Legal obligation to act in client's best interests | Yes, applies to Registered Investment Advisors (RIAs) |

| Suitability standard | Recommendations must be suitable, not necessarily optimal | Applies to broker-dealers under FINRA rules |

Many fee-only advisors register as Registered Investment Advisors (RIAs) with the SEC or state regulators, which legally binds them to the fiduciary standard. This combination of fee-only compensation and fiduciary status creates the strongest structural protection for clients. However, verifying fiduciary status requires reviewing Form ADV and requesting a written commitment. Many investors mistakenly assume all advisors act in their best interests. That assumption is costly.

Commission-based and fee-based advisors operating under the suitability standard are only required to recommend products that are "suitable" for you. Suitable is not the same as optimal. A suitable product might generate a higher commission for the advisor while a better-performing, lower-cost alternative exists. The fiduciary standard closes that gap.

Pro Tip: Request Form ADV Part 2 from any advisor you are considering. This document discloses their compensation structure, conflicts of interest, and disciplinary history. It is free and publicly available through the SEC's IAPD database.

Fee-only vs. fee-based vs. commission-based advisors

The financial industry uses terminology that obscures more than it clarifies. "Fee-based" sounds nearly identical to "fee-only" but describes a fundamentally different arrangement.

Fee-based and commission-based advisors may face conflicts of interest because commission incentives can bias their recommendations toward products that generate higher payouts rather than the best options for clients. This is not an accusation of bad faith. It is a structural reality. When compensation is tied to product sales, the incentive exists regardless of the advisor's intentions.

| Advisor type | Compensation sources | Conflict of interest risk |

|---|---|---|

| Fee-only | Client fees only (AUM, hourly, flat) | Low: no product or trading commissions |

| Fee-based | Client fees plus product commissions | Moderate to high: dual revenue creates potential bias |

| Commission-based | Product sales and trading commissions only | High: revenue depends entirely on transactions |

The practical differences show up in specific scenarios:

- A commission-based advisor recommending an annuity may earn 5% to 7% of the premium as a commission. A fee-only advisor recommending the same product earns nothing from the sale, so the recommendation stands on its own merit.

- A fee-based advisor managing your portfolio may also sell you a life insurance policy that generates a separate commission. The advice on the policy may be sound, but the financial incentive exists.

- A fee-only advisor recommending you hold your current investments and make no changes earns the same fee regardless. That recommendation costs them nothing to make honestly.

Fee-only models support long-term client relationships because transparent fees and aligned interests create greater advisor accountability. Clients know exactly what they are paying and why. That clarity builds trust in a way that embedded commissions cannot replicate.

What to consider when choosing a fee-only financial advisor

The fee-only structure is a strong foundation, but it does not guarantee quality advice on its own. Fee-only compensation reduces conflict incentives tied to trading or product sales, but it does not guarantee expertise or the right fit for your situation. Here is a practical framework for evaluating your options:

-

Confirm they are truly fee-only. Ask directly and in writing. Many advisors use "fee-based" or "fee-transparent" language that implies fee-only status without delivering it. The National Association of Personal Financial Advisors (NAPFA) maintains a directory of verified fee-only advisors.

-

Verify fiduciary status independently. Review Form ADV on the SEC's IAPD database. Look for written confirmation that the advisor acts as a fiduciary at all times, not just for certain services.

-

Match the fee structure to your needs. If you have a $50,000 portfolio and need one-time retirement planning advice, an hourly or flat-fee advisor makes more financial sense than an AUM-based advisor. If you have a $1 million portfolio requiring ongoing management, AUM pricing may be appropriate.

-

Assess service depth and specialization. Some fee-only advisors specialize in tax planning, estate planning, or retirement income strategies. Others offer broad financial planning. Confirm their expertise matches your specific goals.

-

Evaluate communication and compatibility. The best fee structure in the world does not compensate for an advisor who does not understand your priorities or communicate clearly. Ask how often they meet with clients and what their planning process looks like.

Consumers should focus on how advisors are compensated rather than marketing terms when choosing financial advice. The label "financial advisor" carries no regulatory weight. The compensation structure and fiduciary status are the variables that actually matter.

Pro Tip: Search for advisors through the NAPFA advisor directory or the Garrett Planning Network if you prefer hourly fee-only advice. Both organizations require members to meet strict fee-only and fiduciary standards.

Key takeaways

Fee-only model advisors provide the strongest structural alignment between advisor compensation and client financial interests by eliminating commission-based conflicts entirely.

| Point | Details |

|---|---|

| Fee-only compensation | Advisors earn only client-paid fees: AUM percentage, hourly, or flat retainer. |

| Fiduciary vs. fee-only | These are separate standards; verify both through Form ADV and written confirmation. |

| Commission conflict risk | Fee-based and commission-based advisors face structural incentives that can bias recommendations. |

| Inaction as valid advice | Fee-only advisors can recommend holding or doing nothing without losing income. |

| Quality still varies | Fee-only status removes commission bias but does not replace expertise or service quality. |

Why the fee-only model is the clearest path to unbiased advice

I have spent years watching advisors operate across every compensation model, and the pattern is consistent: the structure shapes the behavior, even when the advisor has good intentions. Commission-based advisors are not inherently dishonest. But when your income depends on transactions, you find reasons to transact. That is human nature, not malice.

What strikes me most about the fee-only model is the permission it gives advisors to tell clients what they do not want to hear. "Hold your positions." "You do not need that annuity." "Your current plan is working." These are statements that cost a commission-based advisor real money. A fee-only advisor says them without hesitation because their income does not change either way.

The fiduciary piece is where I see the most confusion among individual investors. People assume that a credentialed, professional-sounding advisor is legally bound to act in their interest. That assumption is wrong for a significant portion of the industry. Verifying fiduciary status is not paranoia. It is due diligence.

My honest caution: fee-only status is a starting point, not a finish line. I have seen fee-only advisors who were mediocre planners and commission-based advisors who were genuinely skilled. The compensation structure removes one major source of bias. Your job is to evaluate everything else: expertise, communication, track record, and whether their planning philosophy matches your goals. Use the client testimonials and references an advisor provides as evidence, not decoration.

— Josh

How Mastermindadvisormarketing helps fee-only advisors grow

Fee-only advisors deliver exceptional value to clients, but that value means nothing if the right clients never find them. Mastermindadvisor.com offers a turnkey marketing system built specifically for independent financial advisors who want to attract qualified prospects without compromising their professional standards.

From educational seminars that position you as the trusted local expert to advisor podcasts that build audience and authority, Mastermindadvisormarketing provides the tools fee-only advisors need to communicate their unique value clearly. Custom CRMs, automated follow-up sequences, and content strategies designed for the financial advisory space mean you spend more time advising and less time chasing leads.

FAQ

What is a fee-only financial advisor?

A fee-only financial advisor is compensated exclusively through client-paid fees, which may include AUM percentages, hourly rates, or flat retainer fees. They accept no commissions or payments from third parties such as product providers or fund companies.

How is fee-only different from fee-based?

Fee-only advisors earn only what clients pay directly. Fee-based advisors earn client fees plus commissions from product sales, which creates potential conflicts of interest that fee-only structures eliminate.

Are all fee-only advisors fiduciaries?

Fee-only is a compensation description, not a legal standard. Many fee-only advisors are fiduciaries, but you must verify this separately by reviewing Form ADV and requesting a written fiduciary commitment.

How do I verify a fee-only advisor's fiduciary status?

Request Form ADV Part 2 from the advisor or access it through the SEC's IAPD database. This document discloses compensation structure, conflicts of interest, and whether the advisor is registered as a Registered Investment Advisor (RIA).

Does fee-only mean better financial advice?

Fee-only compensation removes commission-based conflicts of interest, but it does not guarantee superior advice. Clients should evaluate advisor expertise, specialization, and service quality alongside compensation structure when making their selection.

Recommended

Originally published at source.