Discover the vital role of estate planning content advisors in safeguarding your family's legacy. Learn how they simplify estate planning.

The Role of Estate Planning Content Advisors for Families

Estate planning content advisors are defined as financial professionals who coordinate the financial, organizational, and communication elements of a client's estate plan. They sit between the client and the attorney, translating financial reality into a blueprint that legal documents can actually follow. The Financial Planning Association reports that 41% of individuals first consult a financial advisor when starting estate planning, compared to just 26% who start with an attorney. That gap reflects a fundamental shift. Families increasingly see their financial advisor as the first and most trusted voice in protecting their legacy, not just their portfolio.

What is the role of estate planning content advisors?

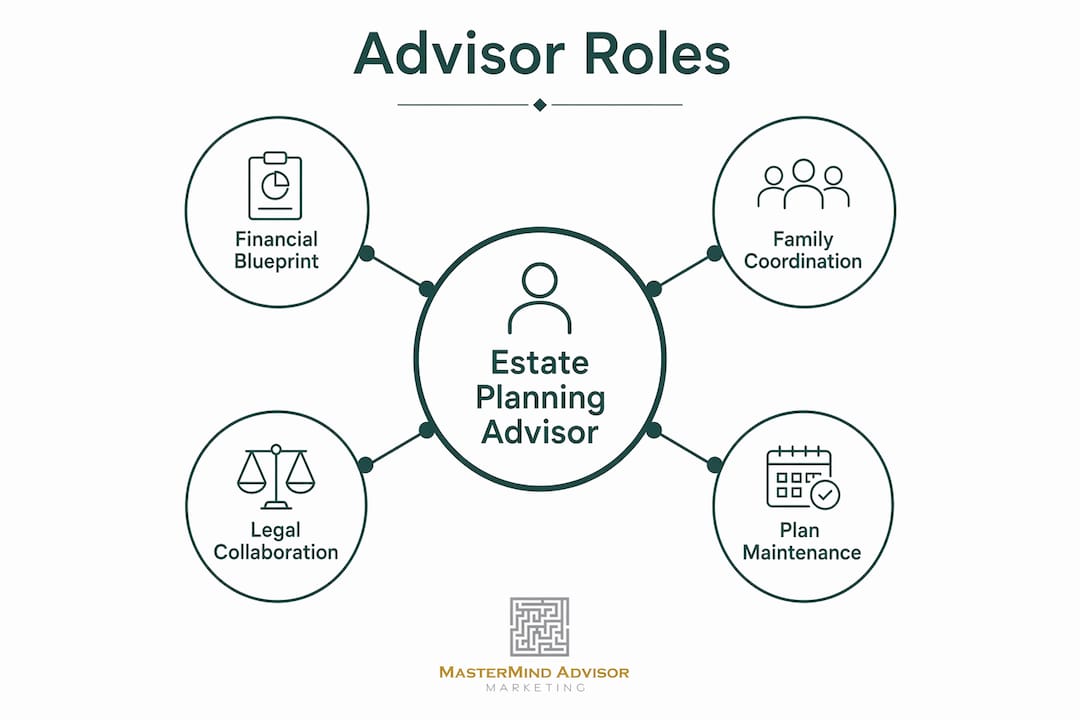

Estate planning content advisors serve as the central coordinators of a client's entire estate planning process. The industry term for this function is "estate planning coordinator" or "wealth transfer advisor," and the role goes well beyond reviewing a will. These professionals map every asset, account, and beneficiary designation to ensure nothing falls outside the plan's reach.

Their core responsibilities include:

- Asset mapping: Cataloging all accounts, real estate, business interests, and insurance policies to identify gaps or conflicts in the estate plan.

- Beneficiary audits: Reviewing and correcting beneficiary designations on retirement accounts, life insurance, and transfer-on-death accounts, since these designations override a will entirely.

- Document coordination: Working alongside estate attorneys to ensure financial accounts align with trust structures and legal directives.

- Life event monitoring: Tracking marriages, divorces, births, deaths, and major financial changes that trigger plan updates.

- Family meeting facilitation: Leading structured conversations between clients and heirs to clarify intentions and reduce the risk of conflict after death.

Non-legal estate planning coaches double plan completion rates by organizing financial details and preparing families before legal document drafting begins. That statistic reveals something most families miss. The bottleneck in estate planning is rarely the attorney. It is the disorganized financial picture the attorney receives.

Pro Tip: Ask your advisor to produce a one-page asset map before your first attorney meeting. It cuts legal drafting time and reduces the chance of a critical account being left out of the trust.

How do advisors and attorneys work together in estate planning?

The distinction between an estate planning advisor and an estate attorney is clear and legally significant. Only licensed attorneys can draft legally binding documents such as wills, trusts, powers of attorney, and healthcare directives. Advisors who cross that line risk unauthorized practice of law. The advisor's job is to build the financial blueprint. The attorney's job is to encode that blueprint into enforceable legal language.

This division of labor works best when both professionals communicate directly. Collaboration between advisors and attorneys prevents conflicting beneficiary designations and closes gaps that neither professional would catch working alone. A trust that holds real estate but excludes a brokerage account worth twice as much is a common and costly error. Direct advisor-attorney communication catches it before the documents are signed.

The advisor brings the financial blueprint. The attorney brings legal enforceability. Neither role replaces the other, and families who hire both get a plan that actually works.

Pro Tip: When selecting an estate planning advisor, ask directly: "Will you communicate with my attorney?" If the answer is vague, that is a red flag. The two professionals must work as a team.

Advisors also stay alert to jurisdictional rules. Estate law varies significantly by state, and an advisor who understands those boundaries protects the client from receiving advice that only an attorney should give. This awareness is a mark of a qualified professional, not a limitation.

Why do families choose financial advisors first for estate planning?

Families choose financial advisors as their first estate planning contact because the relationship already exists. 80% of respondents expect estate planning to be integrated into their financial advisory services. That expectation reflects a demand for continuity. Clients want one trusted professional who understands their full financial picture, not a series of disconnected specialists.

Young families with children under 18 represent the largest group without wills or estate plans, despite having the clearest need for guardianship designations. The barrier is rarely cost or access. It is the emotional weight of confronting mortality and the misconception that estate planning is only for the elderly or wealthy. Advisors are positioned to dismantle both barriers because they already have the client's trust.

Advisors address these barriers through several specific approaches:

- Reframing the conversation: Positioning estate planning as a legacy decision, not a death preparation, reduces emotional resistance.

- Structured family meetings: Bringing heirs into the process early normalizes the conversation and reduces post-death conflict.

- Integrated planning reviews: Embedding estate planning into annual financial reviews makes it a living strategy, not a one-time event.

- Milestone triggers: Using life events like a new child, a home purchase, or a business sale as natural entry points for estate planning discussions.

Behavioral bottlenecks like fear and procrastination are the primary reasons estate plans go unfinished. Advisors who reposition planning as a life event focused on legacy continuity achieve higher completion rates than those who frame it as a legal obligation. That reframing is a skill, not a product, and it is one of the most underrated things a good advisor brings to the table.

For advisors looking to communicate this value effectively, a strong content strategy for advisors helps reach families before they even know they need help.

How do advisors help families implement and maintain estate plans?

Creating an estate plan is the beginning, not the end. Financial advisors act as central coordinators who update plans in response to net worth changes and life events. That ongoing role is where most of the real value is delivered.

A well-maintained estate plan requires these recurring actions:

- Trust funding verification: Confirming that titled assets, real estate, and financial accounts are actually transferred into the trust. An unfunded trust is legally valid but practically useless.

- Beneficiary designation reviews: Checking retirement accounts, life insurance policies, and annuities after every major life event. A divorce that is not reflected in a beneficiary designation can send assets to an ex-spouse regardless of what the will says.

- Heir education sessions: Meeting with adult children or other beneficiaries to explain their roles, responsibilities, and the financial logic behind the plan. Heirs who understand the plan are far less likely to contest it.

- Legislative monitoring: Tracking changes to estate tax thresholds, gift tax rules, and state-level inheritance laws that may require plan adjustments.

- Centralized document tracking: Using digital tools or client portals to store, organize, and share estate documents so nothing is lost or inaccessible at the moment it is needed most.

Professional facilitation of estate planning conversations reduces anxiety and educates heirs on their roles and financial responsibilities. That education function is often overlooked. A beneficiary who does not understand what a trustee does, or why a spendthrift provision exists, is a beneficiary who may challenge the plan in court.

Pro Tip: Schedule a dedicated estate plan review every two years and immediately after any major life event. Set it as a recurring calendar item so it never gets skipped during busy financial planning seasons.

Advisors who use financial services digital marketing strategies can also reach existing clients with timely reminders about plan reviews, keeping the relationship active and the plan current.

Key Takeaways

Estate planning advisors are the most effective first point of contact for families because they coordinate the financial, emotional, and legal dimensions of a plan that attorneys alone cannot manage.

| Point | Details |

|---|---|

| Advisors are the primary entry point | 41% of people consult a financial advisor first, making advisors the dominant starting point for estate planning. |

| Advisors and attorneys serve distinct roles | Attorneys draft legal documents; advisors build the financial blueprint and coordinate asset alignment. |

| Behavioral barriers require active management | Fear and procrastination are the top reasons plans go unfinished; advisors who reframe planning as legacy work achieve higher completion. |

| Ongoing maintenance is where value compounds | Trust funding, beneficiary reviews, and heir education after plan creation prevent the most common and costly estate planning failures. |

| Integrated planning builds client loyalty | Embedding estate planning into annual financial reviews positions advisors as long-term partners, not one-time service providers. |

Why I think most families underestimate their advisor's estate planning role

Most families walk into an estate planning conversation expecting their attorney to run the show. I understand why. Attorneys draft the documents, and documents feel like the product. But after watching dozens of estate plans fall apart in execution, I am convinced the advisor is the more critical player in most cases.

The attorney cannot know that a brokerage account was retitled incorrectly three years ago. The attorney does not sit in the room when a client's adult children learn for the first time that one sibling is the trustee. The attorney is not the one who gets the call when a client's net worth doubles after selling a business and the old plan no longer fits.

Estate planning as a relationship-deepening tool positions advisors as long-term partners who adjust plans through life events. That is the real value proposition, and it is one most advisors undersell. Families do not need a plan. They need a plan that works ten years from now, after three life events they have not experienced yet.

The advisors I respect most treat estate planning as a continuous project, not a deliverable. They schedule the reviews. They call the attorney when something changes. They sit with the heirs. That is what separates a financial planner from a legacy architect.

— Josh

How Mastermindadvisormarketing supports estate planning advisors

Financial advisors who specialize in estate planning guidance need more than expertise. They need a way to communicate that expertise to the families who need it most.

Mastermindadvisormarketing builds turnkey marketing systems designed specifically for independent financial advisors. The platform provides customized webinars, seminars, and estate planning content services that help advisors reach prospects and nurture existing client relationships. Integrated CRM tools and automated follow-up sequences keep advisors top of mind during the life events that trigger estate planning decisions. Advisors working with Mastermindadvisormarketing also benefit from financial services marketing expertise that positions their estate planning knowledge where families are already searching for answers.

FAQ

What does an estate planning content advisor actually do?

An estate planning content advisor coordinates the financial and organizational elements of a client's estate plan, including asset mapping, beneficiary audits, and family meeting facilitation. They work alongside attorneys but do not draft legal documents.

How is an estate planning advisor different from an estate attorney?

Attorneys create legally binding documents like wills and trusts. Advisors build the financial blueprint and coordinate asset alignment to ensure those documents work as intended.

Why do most people start estate planning with a financial advisor?

41% of individuals consult a financial advisor first when starting estate planning, because the existing relationship and integrated financial view make advisors the most natural starting point.

How often should an estate plan be reviewed?

An estate plan should be reviewed every two years and immediately after major life events such as marriage, divorce, the birth of a child, or a significant change in net worth.

Can a financial advisor give legal advice on estate planning?

A financial advisor cannot give legal advice or draft legal documents. Only licensed attorneys can perform those functions. Advisors who cross that line risk unauthorized practice of law.

Recommended

Originally published at source.